- Step 1: Authenticate the Client's Identity

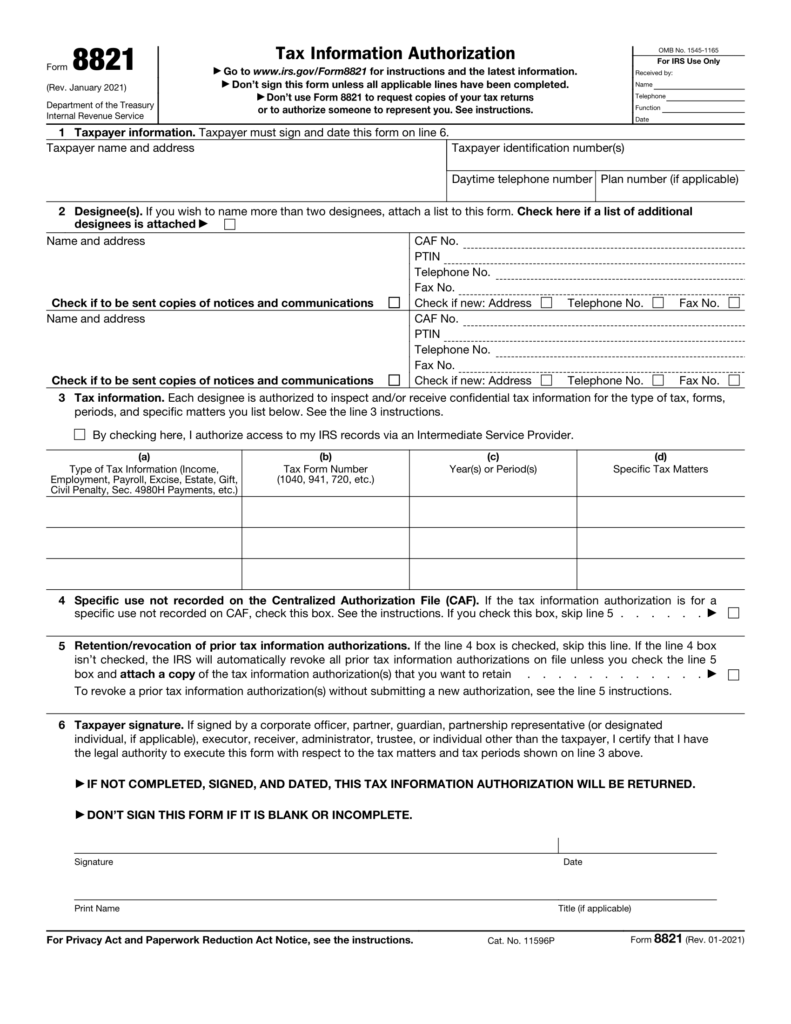

- Step 2: Enter Taxpayer and Designee Details

- Step 3: Designate the Type of Tax Information

- Step 4: CAF Recording and Prior Tax Information Authorizations

- Step 5: Sign and Date the 8821 Form

- Step 6: Submit the Completed IRS Tax Form

Form 8821 Vs. Form 2848

Form 8821 only allows access to certain taxpayer information. A designee with access cannot perform any actions on behalf of the client, and they do not need to meet any specific eligibility requirements.

Form 2848, on the other hand, grants the representative power of attorney (POA) and allows them to represent the client before the IRS. A representative appointed through Form 2848 could, for example, sign a tax return or other tax-related documents on your behalf.

While their powers are limited, representatives with POA through Form 2848 have much greater access than those appointed using Form 8821. The IRS, therefore, requires individuals to meet certain criteria if they wish to represent a client using Form 2848.

When to File Form 8821

If you need to submit Form 8821 to allow the IRS to share your private tax information for a reason other than dealing with a tax-related issue (such as verifying income for a lender), you must send the form to the IRS within 120 days of signing it. However, this 120-day rule does not apply if you are submitting Form 8821 to authorize disclosure for help with a tax matter with the IRS.

How to Fill Out Form 8821

The form must be complete and accurate to be valid. Any oversights can cause significant delays. Follow these instructions to complete the process successfully.

Step 1: Authenticate the Client’s Identity

If you are filling it yourself, skip this step. If you are a tax professional or completing Form 8821 on behalf of an individual, confirm their identity by checking a photo ID, passport, or social security card.

For a business or other organization, obtain their federal Tax ID or employer identification number (EIN). Then, verify the representative’s identity and confirm they have permission to act on behalf of the client organization.

Step 2: Enter Taxpayer and Designee Details

Enter the full name, mailing address, phone number, and social security number or tax identification number for the taxpayer and the designee(s) on lines 1 and 2. Note that you can name more than one designee. Enter the designee’s Centralized Authorization File (CAF) number, a unique nine-digit number assigned by the IRS to parties requesting third-party authorizations.

If your designee has a CAF number from a previous Form 8821 or Form 2848, use it. If not, enter “NONE,” and the IRS will assign one. Note that CAF numbers are not assigned for employee plan status determination or exempt organization application requests.

Step 3: Designate the Type of Tax Information

Indicate the type of tax information the designee can access. This may include tax information for income taxes, employment taxes, excise tax, payroll tax, and more.

State which tax forms the designee can obtain and the years or time periods they can request. Detail the specific tax matters for which the designee requires each document. For example, you can list “Income, 1040” for the calendar year “2021” and “Excise, 720” for the same year (covering all quarters in 2021).

Avoid using general references like “All years,” “All periods,” or “All taxes,” as they will not be accepted. If you need to include multiple years or a series of inclusive periods, including quarterly periods, you can enter “2018 through 2021” or “2nd 2019–3rd 2020.” For fiscal years, please enter the ending year and month in the format “YYYYMM.”

Step 4: CAF Recording and Prior Tax Information Authorizations

Most tax records and authorizations are recorded in the IRS CAF system. However, certain uses are exempt from being recorded. Check the box on line 4 if your Form 8821 is for non-recorded use, as indicated by the IRS.

If you do not check the box on line 4, the IRS automatically revokes previous authorizations for tax information unless you request otherwise. You can request that previous authorizations remain intact by checking the box on line 5.

Step 5: Sign and Date the 8821 Form

Once you have completed the form, the taxpayer should print their name and title (if applicable), sign the form, and enter the current date. The IRS will reject the form if it is not completed, signed, and dated.

Step 6: Submit the Completed IRS Tax Form

You can submit your completed and signed 8821 form to the IRS by mail, fax, or through the IRS’s new authorization tool. Check the IRS Where To File Chart to determine the correct fax number or mailing address for your state of residence.

You cannot mail or fax an electronically signed Form 8821 to the IRS. Mailed or faxed forms must have a “wet” ink signature.

Form 8821 Sample

Download a fillable IRS Form 8821 template in PDF format.

Create Your IRS Form 8821 in Minutes!